The Range of Possible Economic Outcomes is Wide. Diversification is Key

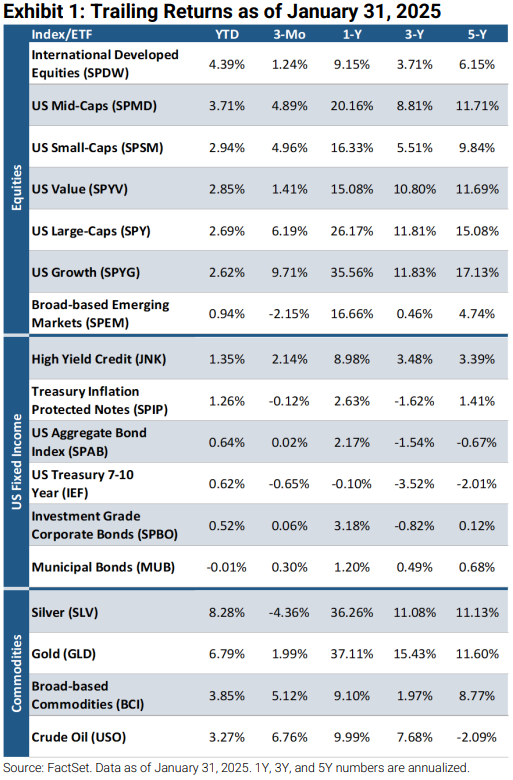

Equities Post Another Record Month

Despite tariff concerns and an AI scare driving the bid for safe haven assets towards the end of the month, strong earnings and consumer spending drove another positive month of equity returns in January. The S&P 500 Index closed the month at another all-time high despite volatility. International developed equities (+4.4%) were among the best performers, followed by US mid-caps (+3.7%) and US small-caps (+2.9%). Bonds were mostly up as high yield credits increased 1.4%, Treasury inflation protected notes gained 1.3%, and the US Aggregate Bond Index rose 0.6%. Commodities were among the best performers, with silver and gold at 8.28% and 6.79% respectively, with broad-based commodities (+3.85%) and crude oil (+3.27%) also producing notable returns.

Fed Pauses, Proceeds with Caution

At the January FOMC meeting, the Federal Reserve chose to pause rate cuts, keeping the fed funds rate at the 4.25–4.50% range. This marks a shift from easing over the last few months. The Fed’s decision reflects its more cautious stance amid ongoing, though decreasing, inflation pressures and a still strong economy. While inflation has come down from its peak, it remains above the Fed’s 2% target, and the central bank emphasized its commitment to monitoring economic conditions closely. However, policymakers indicated they foresee fewer rate cuts ahead, signaling that the era of aggressive easing may be over for now. The updated Summary of Economic Projections reflected this more measured approach, with the Fed now forecasting fewer rate cuts in 2025 than previously expected. The dot plot showed the potential for one or two cuts, down from earlier expectations for more substantial easing. Currently, an 86% chance of no change in March is priced in per the CME FedWatch Tool.

Mag 7 vs. S&P 493 Net Income Growth

In prior years, the Mag 7 outperformance was justifiable from an earnings standpoint. However, the rate of change in earnings has declined while the 493 is expected to marginally increase. Diversification will be paramount this year. NVDA lost nearly $600 billion in market cap in one day. Investors may want to think about capping the weights in their portfolios.

GDP Estimates Revised Higher

As of February 3, the GDPNow model projects real GDP growth at an annualized, seasonally adjusted rate of 3.9% for the first quarter of 2025, an increase from 2.9% on January 31. Following recent data from the Institute for Supply Management and the US Census Bureau, the forecasts for first-quarter growth in real personal consumption expenditures and real gross private domestic investment rose from 3.0% and 4.8% to 4.1% and 6.5%, respectively.

US Retail Investor Shows Strength

Per JPMorgan, in the past week, retail traders net bought over $8 billion in equities, the largest weekly inflow in two years.

The Range of Possible Economic Outcomes is Quite Wide. Diversification is Key

The economic recovery has been stronger and longer than most expected. We have conviction in pockets of the market, but concentration risk and high multiples remain an issue for large caps, and there are looming risks such as geopolitical tensions, and inflation concerns centered around policies such as tariffs. The distribution of outcomes is wide in 2025, and diversification will be key. Astoria prefers to invest in areas of the market we believe are more undervalued, as opposed to large-cap index funds, especially with bond yields at risk of moving higher.

In our 10 ETFs for 2025, we wrote this is a once-in-a-decade opportunity for US small caps. Using a median multiple, small-caps trade in the bottom 35th percentile, while large-caps trade in the top decile. As previously mentioned, the S&P 493 earnings are projected to steadily increase by year-end.

We like idiosyncratic investments like US banks, data centers, powerplays, and equal weighted strategies. Additionally, real assets, which historically have been effective inflation hedges, are trading at approximately half of the S&P 500 valuation.

On the fixed income side, US rates continue to be range-bound; keeping duration short is advisable. With credit spreads tight investors should look to be selective with bonds. We think the long-term debt cycle poses a systemic risk for 60/40 portfolios. Mortgage-backed securities look attractive with spreads of ~129bps and in the 79th percentile, whereas the US investment grade spreads are 88bps and in the 7th percentile.

Warranties & Disclaimers

There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements.